As we step into 2025, the realm of Environmental, Social, and Governance (ESG) is poised for transformative changes. From expanding regulatory frameworks to heightened supply chain scrutiny and risks and the increasing importance of assurance, the ESG landscape is evolving rapidly. Additionally, the integration of artificial intelligence presents both opportunities and challenges that demand a delicate balance between innovation and sustainability. This article explores these top ESG trends to watch in 2025 providing insights into how businesses can navigate these developments to stay ahead and meet stakeholder expectations.

Regulatory Expansion

In 2024, the first group of companies faced the EU’s daunting Corporate Sustainability Reporting Directive (CSRD). As the calendar turns, a new cohort that includes EU-based firms that meet two of the following three criteria: have turnover exceeding €50 million, a balance sheet total of more than €25 million, or more than 250 employees averaged over the year will begin reporting. Many of these companies, unlike the first cohort, do not have the benefit of experience reporting against the rule the CSRD replaced, the Non-Financial Reporting Directive (NFRD) as a foundation.

Over in the United States, California has enacted regulations that will require large businesses to disclose climate-related financial risks and greenhouse gas (GHG) emissions in 2026 based on the fiscal year 2025 data. While the nationwide SEC rule remains on hold for the foreseeable future, access to California’s $3.9 trillion economy is enough incentive for many companies to comply with the new requirements.

Elsewhere, there’s a growing global trend of regulators adopting the International Financial Reporting Standard’s (IFRS) S1 and S2 disclosure standard for their jurisdictions. Australia and Singapore have already committed to mandating disclosure of 2025 sustainability data based on these standards while the UK, Canada, and Japan, to name a few, have expressed their intent to implement similar measures.

Many IFRS S1 and S2 adoptions by regulators have slight alterations that make them more relevant to their governing jurisdictions. Companies that may need to comply should look to the regulating bodies, specifically, rather than assume uniformity with ISSB.

For more specific details on how sustainability disclosure regulations are changing in 2025, check out our Global Sustainability Regulations Guide for 2025.

Supply Chain Risks

Supply chain and distribution networks and vendors are always top-of-mind in today’s economy.

While partner cost, speed, reliability, and adaptability are critical balance sheet supplier measures, stakeholders also increasingly demand sustainability, ethics, and corporate responsibility transparency across supply chains.

Key Supply Chain Risks

Businesses must assess risks factors and their resilience against unpredictable climate disasters, changes in natural resource availability, and carbon tariffs like the EU’s CBAM that can not only disrupt their operational strategies but their reputations as well. Investors and customers want to know this as well – is the business reliable or is it vulnerable to climate-related risks in its supply chain? Stakeholders tend to penalize companies for uncertainty.

Consumer preferences also play a large role in transparency demands. The global consultancy Simon-Kucher found in its 2024 sustainability consumer study that 64% of consumers rank sustainability as a top 3 value driver in purchasing decisions and nearly 70% perform research on brands’ sustainability claims. As these consumer trends grow, lack of reliable sustainability data becomes a liability not only for consumer brands, but for business-to-business (B2B) revenue as well.

Scope 3 Reporting Transparency

Some of the biggest downstream impacts of regulations like CSRD and the California climate laws stem from their requirements to disclose indirect GHG emissions, categorized by the GHG Protocol as Scope 3. These requirements of large companies permeate throughout the supply chain placing demands on smaller businesses that don’t face such regulatory scrutiny directly.

While there may be some leniency today due to reporting costs and lack of expertise with smaller enterprises, their leashes are shortening. Large companies will look for partners that can provide adequate sustainability data that can help them maintain compliance. Sustainability questions are becoming more common on RFPs, so companies can more accurately understand risks they face with partners and select a preferred vendor when there are limited differentiating factors otherwise.

B2B Customer Demands

Walmart, as a company with a particularly extensive supply chain, has been a successful case study in galvanizing its partners to improve sustainability transparency around a specific goal. Walmart began its Project Gigaton back in 2017 to engage suppliers in climate action and reached its goal of reducing or avoiding one billion metric tons of GHG in 2023 by engaging, educating, and providing resources for more than 5,900 suppliers.

Other large companies and consortiums are taking note and developing their own programs to reach ambitious sustainability targets. Some companies approach this through common goals and reinforcement while others take more punitive measures that demand supplier transparency as a contingency to continue their partnerships. We expect to see both types of initiatives expand and mature in 2025.

Potential Impact of Tariffs

The incoming Trump presidential administration in the US has been vocal about its intent to increase tariffs on imported goods. Businesses will need to assess the impact of these new taxes, which includes gauging sustainability-related risk factors of different production countries and understanding if reshoring will have an improved cost-benefit analysis. Offshoring has historically been a cost-motivated activity as it tends to lengthen lead times, increase shipping risk, decrease adaptability to consumer trends, and weaken reputation. While the first Trump administration’s tariffs (mainly left unchanged by the Biden administration) largely shifted production to countries like Vietnam and Costa Rica from China and Mexico, broader tariff application could upend supply chain strategy.

Companies that do move operations in response to changing import and export costs will need to measure and forecast how these shifts will impact their sustainability commitments and long-term targets.

Reporting Integrity Takes Center Stage

Growth in ESG Assurance

The rates in which organizations have attained assurance for their sustainability and ESG disclosures have steadily grown over the past few years. Studies from the International Federation of Accountants (IFAC) and the Center for Audit Quality (CAQ) found notable growth in assurance from 2020 to 2022 across global firms from 58% to 69% and in the S&P 500 from 61% to 70%, respectively.

Both studies found the proportion of US companies studied that opted for reasonable assurance versus limited assurance to remain flat – about 18% based on IFAC sample and 13% of S&P 500 from CAQ. The CAQ did observe, however, the number of S&P 500 companies obtaining reasonable assurance doubled in 2022 to 62 from 31 in 2021.

The growth trends of both overall assurance and reasonable likely stem from greater sustainability reporting maturity across businesses and heightened pressure from investor groups for CDP disclosures, and the reputational benefits of receiving an A-rating with its assurance requirement.

The rate of assurance growth will likely continue to outpace the rate of assurance maturity in 2025 for a few reasons.

- Limited assurance is a requirement for CSRD and the California climate laws with reasonable assurance expected to begin phasing in in 2028 and 2030, respectively.

- Most voluntary incentives, like a CDP A-rating, require assurance in general versus distinguishing reasonable assurance.

- Hard costs (SEC 2022 median audit cost estimate $75,000-$175,000) and resource commitments of reasonable assurance are higher without much perceived benefit over limited assurance (SEC 2022 median audit cost estimate $45,000-$110,000).

When the costs outweigh the incentives and the demands do not exist, companies will continue acting with prudence avoiding the extra scrutiny and resource requirements of reasonable assurance.

Beyond Spend-Based Scope 3 Carbon Accounting

While regulators and voluntary standard setters generally accept all methods of Scope 3 GHG calculations from the GHG Protocol, businesses are facing demands from their customers and investors to utilize more accurate methods. Enterprise corporations, in particular, are being asked for more accurate Scope 3 measures, which trickles down through their supply chains and the products they purchase.

“We’ve seen significant demand increases for product-level carbon footprint data in the past year,” shares IsoMetrix Sales Director Kevin Ferris. “Regulatory pressure is only part of the story, and other stakeholders are demanding greater data confidence without the procedural hurdles governments face.”

This aligns with feedback the GHG Protocol received in a recent Scope 3 stakeholder survey that many were dissatisfied with spend-based carbon accounting. Stakeholders proposed a range of suggestions including creating a calculation method hierarchy that would likely rank spend-based lower than other methods, developing contingency factors that would essentially penalize lower quality calculation methods, and even phasing out spend-based entirely.

Obtaining reliable product-level data is still a costly practice and prohibitive for many smaller businesses. This trend may have been on the fringes in 2024, but we expect it to gain momentum as the threat of losing customers becomes more real.

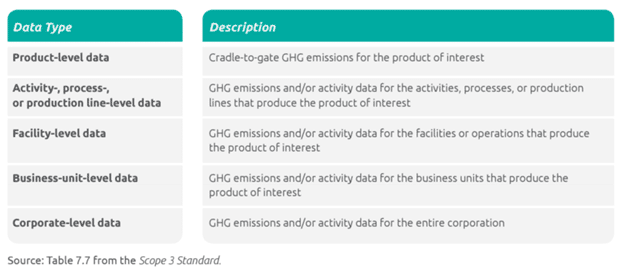

Scope 3 Levels of Data (Ranked in Order of Specificity)

The AI Balancing Act

Greater Power Demand

Artificial Intelligence (AI) technology’s demand for computing power and energy has been widely covered over the past two years as its application and adoption skyrocketed. Microsoft’s electricity usage more than doubled from 2020 to 2023 with its CO2 emissions growing by more than 40% over the same period. Microsoft, Google, Amazon, and Meta have all announced their intents to invest in nuclear energy as a source of reliable clean energy to reduce the climate impact AI causes with its increased load on electric grids to power data centers.

Every company is looking for ways to capitalize on AI’s widespread availability, but not every company will see the level of energy use increase that demands explicit and intentional mitigation to balance computing power demands. The energy costs of AI will continue to capture attention and scrutiny in the big tech circles. It won’t be a surprise if companies begin reporting avoided emissions attributed to AI in 2025.

Applicable AI Use Cases for Sustainability Reporting

Chat GPT is not at the point yet where it will create a full sustainability report for your business from a pool of unstructured data spread across the business, but there are a few time and cost saving applications that will harness AI’s ability to work with large volumes of data efficiently when it comes to sustainability reporting and risk management.

- Anomaly Detection: Application of learning models to flag anomalous data for review, alerting managers of potential data entry errors or problematic areas that may need remediation.

- Key Driver Analysis: With good data, AI can circumvent human biases to identify and apply data science models to uncover correlations, root causes, and leading indicators in risk management, especially when it comes to environment, health, safety, and stakeholder engagement monitoring.

- Natural Language Summarization: Condensing large volumes of data into actionable insights for leaders to develop more informed strategies in shorter time.

- Predictive Forecasting and Scenario Modeling: Forecasts and scenario models often demand significant time and effort from experts to develop. Even then, positive or negative biases come into play when humans predict future outcomes. AI can rapidly generate models to provide expected ranges with less bias.

- Risk Warnings: Nature and climate disasters are predictable to an extent with the likelihood and disruption potential calculated in geospatial and meteorological models. When disaster likelihoods are miniscule, however, preparation can be difficult to budget. AI has the ability to connect indicators for earlier warnings to give people and communities more time to prepare when a 100-year climate disaster does occur.

As these trends unfold, companies that stay ahead of the curve will be better positioned to navigate the evolving ESG landscape and meet the expectations of stakeholders. Keep an eye on these developments to ensure your organization remains compliant, competitive, and committed to sustainability.

Find out how IsoMetrix can help your business meet growing expectations across stakeholder groups, reduce risks, and improve sustainability reporting confidence.